1. Application of computing in business has grown in expanse and depth very rapidly and added lots of new dimensions in operations, service delivery and business management. Analytics is one such specialised area that can be used to enhance customer experience as well as business manager’s capabilities for directing business efforts with focus. When you call a marketing site and get answered in your preferred language with greetings by name, reckon that analytics have played in the background. You look up a marketing site to view some preferred items , say a TV for example; next time you go to your mailbox to check for emails, advertisements appear here and there on the screen , about those preferred TVs and brands- click it and you are in the marketing site with the specific item on the screen. Surely analytics is playing a part in all these.

1. Application of computing in business has grown in expanse and depth very rapidly and added lots of new dimensions in operations, service delivery and business management. Analytics is one such specialised area that can be used to enhance customer experience as well as business manager’s capabilities for directing business efforts with focus. When you call a marketing site and get answered in your preferred language with greetings by name, reckon that analytics have played in the background. You look up a marketing site to view some preferred items , say a TV for example; next time you go to your mailbox to check for emails, advertisements appear here and there on the screen , about those preferred TVs and brands- click it and you are in the marketing site with the specific item on the screen. Surely analytics is playing a part in all these.

2. Data volume gets very big in today’s human activities at business, say like banking, because business delivery and customer operations are on computer, in almost all activities – which means much more information on customer activities are getting captured in computerised environments, leaving trails and records in terms of computerised records. To be able to understand and direct business efforts internally, or, provide rich and meaningful components and contents in customer interactions, all such data related to customer transactions and behaviour, as also external environmental / market data, are required to be captured, understood, studied and analysed. From all such data, selected portions are extracted, suitably restructured for ease of quick retrieval to help in queries made on this big pile of data, and combined into new data elements forms a new and different database. This process is ETL – Extract Transform Load. These information of different items or activities etc., are then put in a different database ; these databases form the base of the activities like storing of information, retrieval and processing to discover trends, rules, patterns of customer behaviour and some more related information. The various types of activities and handling in this area are termed as Data mining, Data Mart, Master Data Management, etc. Under the overall domain of Data Warehouse. Structured and organised data are made of data elements that follow strict rules of length, content type, permissible range of values, etc. However, there will be much other information which may be in texts, pictures, sounds etc. that may be useful to study and rate. For example, apart from price, a design or colour shade of merchandise, may have reasonable influence on customer preference without customer being able to articulate the same. However, by studying customer preferences, the back end system of a seller can have an insight to use for production and marketing strategies. This class of data will not follow a fixed structure, syntax, size or even the form – these constitute what is called ‘unstructured data’.

After we have these data, i.e., original business data and then reconstructed as mentioned above, we need to analyse them to find meaningful insight. This part of activity is Analytics. There are other activities after this to use the findings for internal understanding, relate such findings to the business facts observed (proposing models and testing them for validation), rating of various factors so found and create and test business strategy, customer interaction, marketing strategy etc. Incidentally, always a customer or selling a merchandise, are not the target of the exercise. We bankers may do an Analytics of our MSME loans portfolio, study the repayment histories, the appraisal and sanction procedure, post sanction acts of bank, market conditions, overall external indebtedness of borrower, family earning and loan histories etc.,

to perhaps arrive at a desired accurate formula for making provisions for bad loans. Because the data is diverse and huge - thumb rules or simple averages or projections based on one or two easily measurable factors, will not do. And, if we desire to know while doing a Money Market deal, probability of this deal to cause the bank to exceed any agreed risk exposure level or limit at the whole bank level, then the Analytics and the resulting action have all to be real time, within the activity session of the deal. The narrations above are of course a simplified and narrow bird’s eye view only, the gamut of activities and challenges to understanding data in reality, are much bigger and difficult.

3. Analytics as a part of the integrated data driven operations of an organisation, will usually consist of classifying, segmenting, grouping of data, computing some values (of result, trend, etc.) representation of the same on screen by tables, charts and graphs of different types, dashboards, scoring tables, or similar any other graphic ( for on- screen) presentation providing interactive program for business management to study, change a few parameters and see the effect on the result, etc. For example, we can see the impact of a change in, let us assume, transaction charges to be levied for services - - by trying with various different values of transaction charges, and note the expected changes for the same on the profit or market share; this can be as a graph or bar chart or any other desired format of output on screen that appear about immediately (after entering the varying inputs). This class of activities are often called ‘what-if” exercise. The practice of visually seeing a change in output as an impact of complex business factor interplay, - is called Visual Analytics. Sometimes depending on the domain or platform to be studied or evaluated , a genre of analytics is named – e.g.– Cloud Analytics, Banking Analytics, Risk Analytics, Loan Analytics, in commercial communication. Basically selection of parameters to study, the data elements to be chosen, the features of the output, the business domain specific data elements, and the format of the result to be shown – may often have some specialities or usage norms; they use business rules and concepts of that domain, and can get bundled and sold under such specific names like in the foregoing example; there are no hard and fast rules however.

The major target of analytics is to understand the dynamics of market factors, operational entities, etc., and then be able to predict market response or customer impact, and then finally to provide suitable links, handles, offers in customer interactions in terms of presentation of the interactive internet screen for customer; the customer can be internal – (like in our example of the loan portfolio understanding above)

– who are expected to invoke a favourable action – (like customer gets enthused to purchase an item). With such results for a larger number of sample of customers, the internal team may get helped to select or propose the underlying algorithm and build up a model for implementation and testing The types of analytics that are specifically tailored to predict results or outcomes to help business plans and strategies, have grown into a distinct genre and are referred as Predictive Analytics. As mentioned above, there are many other typenames based on purpose or business domain (Financial Analytics, Big Data Analytics, Customer Analytics for banks, Risk Analytics for banks – which are termed and marketed as specific products by vendors to service providers / banks / business) or on similar segmentations. The major driving forces behind banks going in for analytics may be a few – most notables are:

a. Regulatory Reforms, asking for more and more data based information from banks.

b. Profitability/ Cost cutting in view of increasing competition.

c. Achieving Efficiency in operations.

d. For better Risk management.

e. To obtain better insight into business data and customer preferences – these can be customer segment-wise also, providing a farther segmentation.

f. Attempt to redesign business processes.

g. Fraud Control.

h. Loan delinquency avoidance.

i. Customer satisfaction assessment and enhancement.

j. Call centre or workforce efficiency.

k. Cross selling, customer acquisition, etc.

Hardly, an all pervasive project to kick-start many studies and activities in many domains will get done simultaneously, because business dependence is complex based on multiple factors. Any model or strategy, should better be piloted and tested in parts, by adjusting different parameters one by one, and the overall business system allowed to grow with these, in steps of changes to help stabilisation and correct understanding of effects of a change in each of the many factors in a business situation.

4. Banks handle huge data, and need to do more, which they may not be normally doing – say for example while we study loan defaults on the basis of accounts or customer numbers; however, study of relationship of loan delinquency with customer’s family/lifecycle issue history or projected competition of alternative service providers that may affect banking usage of customers, etc, is not easy, as, dependable data itself may not be there, or their relationship to business results are not understood well. Over and above, the thinking and capabilities required for data crunching and finding patterns in huge volume of data, are not in the core competence areas of bankers. On the other hand, technocrats are not expected to have the business domain knowledge. In this backdrop, it may be appropriate to see how best a simple banker can get along with Analytics in the best interest of the organisation.

5. The various available products of Analytics in the market as they are, suggest that the developers behind them have gained a reasonable insight in the underlying business. The teams of technology experts and business process experts from the providers’ sides have developed these products. The most distinguished and established organisations like Gartner or Forrester rate the capabilities of vendors that get accepted more than for any other ratings in the industry. These ratings tell us company-wise capabilities based on various factors that they explain in these rating releases. However, if we bankers plan to consider a specific genre of product, it will be good to look into the views on the particular product and domain and check that the functionalities and deliverables are in line with what is our plan and our own domain. We may not at the outset, be able to spell out or fully plan the outputs or the resulting product to procure, like we can normally do when we procure a server or few discs or some equipments, or some fixed functionality products like MS Office, etc. There will be some exploratory components in the solution and the outputs. There can be a facility in the solution provided - for user operated (by the banker who is implementing this solution) day to day analysis, report, parameter changes, etc., on a regular basis, or as and when required. It may be useful to adopt a few core outcomes, like capacity addition for understanding/analysing / reporting etc for management support, as the desirables; specifics of the solution can get defined and refined as we go from here. The banker’s team involved in the initiation of the specific analytic must have members knowledgeable in the business process of the underlying specific business area operations, for which an analytic solution is planned to be deployed. In most of the situations, the analytics vendors (that include big names like SAS, IBM ,etc worldwide, as also quite a few niche solution providers are there in the top bracket) have, through the assignments handled, collected knowledge and practices of the business domain and embodied the same in their solutions. So, as such many vendors would be approaching banks with specific solutions – say on credit risk management, or fraud risk management, etc. These are to some extent ready, that a bank can procure, learn operations, put values of parameters, get trained in, and start. This may prove to be a very easy and comfortable option for a functionary in the bank side, because, depth of their expertise or conceptual clarities may not be very great always, due to frequent movements in banks or limited or no experience, or also, the areas are new and growing, or, scope of theoretical grounding and exposure to global knowledge and practices are limited. Whatever it maybe, these together may lead to a situation of vendor dependence for operating expertise and also, thought leadership, This may not be helpful for knowledge enrichment and capacity creation in the bank. It is a good idea to expose the bank team for an analytics task / project, to theoretical concepts and industry best practices- preferably in the domain desired to be controlled or predicted with Analytics. For example – if we need to take up an analytics exercise to find what all to do to improve capital adequacy and block and mitigate factors that erode capital adequacy, even if a vendor arrives with a ready model and solution to fit into – it will be useful to field a team from the bank side consisting of business domain people thoroughly knowledgeable in the concepts of capital adequacy, Basel committee norms and directives, RBI directives, models in industry use in this field, etc., testing and validation concepts like stress testing and other global practices, and also internal working in the bank to the extent that covers how from all the business departments practically which business figures and data emanate and get fed into required capital adequacy computations, and, to what extent. The team also should have one or two Information Technology person(s) who are thoroughly conversant about which data elements pertinent to this domain are sourced from which accounts or operations in IT, if there are processing issues in IT that may have scopes to have bearing on the data values (say some values are repeated from old data if new data is not updated and some others are left blank if new data is not received – the dependability of the data quality gets differently affected in these two cases), and similar inside views. The IT persons are also to act as bridges with IT for interfacing or aligning any analytics input or output from or to the main banking system (core banking) or its subsidiary systems. Apart from proper manning and business knowledge gathering on the issue to be subjected to an analytics exercise, the usual project management that the banks do, often in their own practiced ways – will have to be in place as usual for the analytics project also. However, Analytics being a bit advanced in concepts and far more advanced in IT- in terms of processing capabilities and methods than the usual applications that get added besides corebanking, the processing of the analytics activities are to be in the analytics technical domain mostly. However, we need to have some insight and some understanding in gross terms, about the working models and components of analytics.

In most cases, analytics should lead to Predictive Analytics that should predict outcome (example - in which case the chance of a borrower failing to repay will become high), and suggest actions and produce the appropriate actionable (say a special notice to borrower, or, a special inspection schedule for the loan officer can be produced by the system, or the account can be included in providing for doubtful accounts to a decided extent) , and very desirably- the system should automate the process to a good extent – leaving it for human approval or revision

if desired. The basic purpose is to use superior technical capabilities with control and focus on business goals – not getting overwhelmed or led by technology. Also, providing clean data, appropriate data, data that can be verified to be correct – are very important, as otherwise analysis, modelling, and predictions based on such information will not be useful to business. For the analytics to be useful, the banker is primarily responsible to have clean and correct data in the system. This sounds obvious, but is hardly come across. Incorrect, incomplete, and inconsistent data has been there to an unacceptably high proportion in many banks. Rapid expansions, conversion from manual to branch-based computerisation and thereafter to core banking could not take care of these gaps fully because the older systems and the later systems did not have the same data elements, and often the older data elements were not captured at one place so that many gaps resulted while converting to later versions. Banks have through special drives of data cleansing and de-duplication covered some ground. However, for a particular group data to be adopted for Analytics to provide us with insight and suggest actions –the first requirement will be a special check and cleaning of the data, as also, conscious decisions as to what default rules will apply in case of inconsistency, the actions to be taken for them, and the impact of these imperfections on the results should be understood, and used while appreciating the Analytics outcome.

6. Before coming back to the issue above, it may be useful to again understand the gamut of use of data for business understanding and directions and the entire universe of data warehouse, data mart, Business Intelligence, analytics, visualisation, modelling, predictions, etc., to understand the place of analytics in these and its role.

a. Gartner defines Business Intelligence (BI) to be a wider activity that “spans the people, processes and applications/tools to organize information, enable access to it and analyze it to improve decisions and manage performance” In this context Analytics is defined as “packaged BI capabilities for a particular domain or business problem” [Gartner IT Glossary]. Other definitions put Analytics as a science of analysis, or, tracing of

things to their source, or mapping information to its original causes or principles. In other words, analytics is a way to understand causes of and connections among business events, business conditions, outcomes. So, analytics is expected to enable business managers to appreciate causal relations that are not easily visible, lead to insights some of which may be found to be crucial or significant. This leads to right business decisions that are difficult to derive in normal course in view of the usual deluge of multidimensional information faced in business from diverse sources.

Abstract:

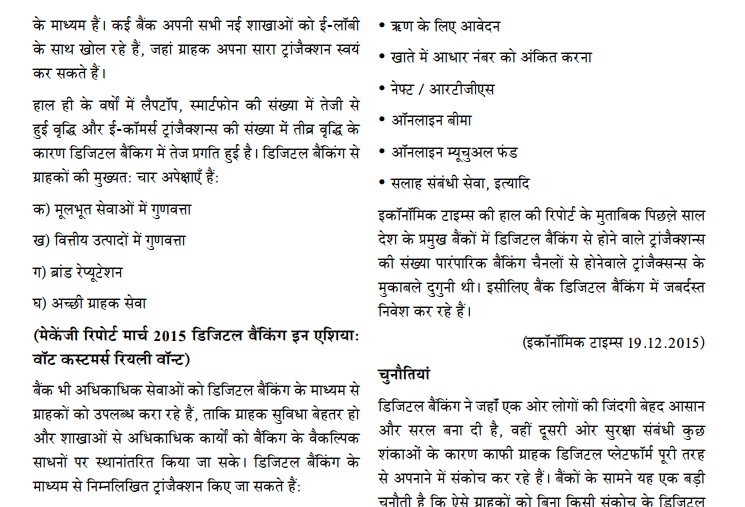

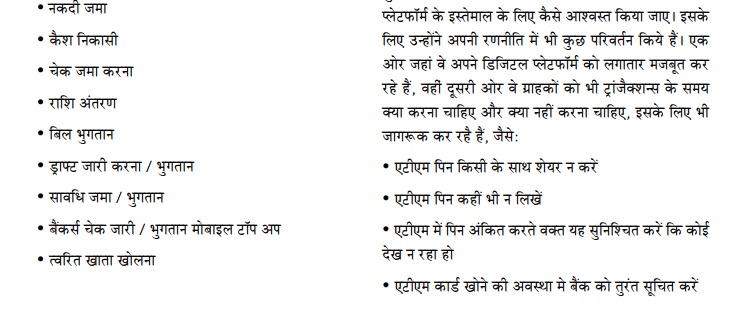

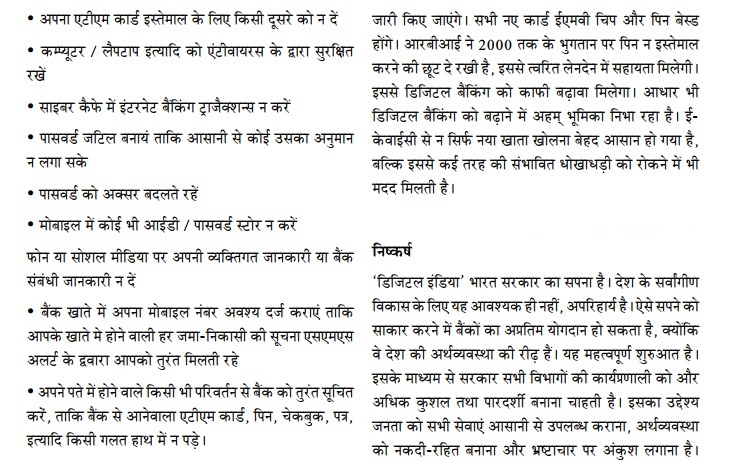

Abstract: तकनीक, जोखिम और परिवर्तन को एक ही सिक्के के दो पहलू माना जा सकता है। इतिहास गवाह है कि दुनि या के तमाम बड़े परिवर्तन बदलती आवश्यकता के परिप्रेक्ष्य में समय, तकनीक एवं आवश्यकता के समन्वय के आधार पर हुए हैं और अधिकांश परिवर्तनों के साथ मानवीय सुविधा एवं समन्वय जुड़े हुए होते हैं। बीते दशक की बैंकिंग भी इन ऐतिहासिक बदलावों, परिवर्तनों से अछूती नहीं रही है। यह बैंकिंग तकनीक में आए बदलाव का ही असर है कि आज बैंकिंग सेवा किस ी-न-किस ी रूप में 24x7 उपलब्ध है। इन बदलावों, परिवर्तनों से बैंकिंग सेवा में हर रोज नए बदलाव परिलक्षित हो रहे हैं, जिससे आम जनता के साथ-साथ देश की अर्थव्यवस्था भी लाभान्वि त हो रही है।

तकनीक, जोखिम और परिवर्तन को एक ही सिक्के के दो पहलू माना जा सकता है। इतिहास गवाह है कि दुनि या के तमाम बड़े परिवर्तन बदलती आवश्यकता के परिप्रेक्ष्य में समय, तकनीक एवं आवश्यकता के समन्वय के आधार पर हुए हैं और अधिकांश परिवर्तनों के साथ मानवीय सुविधा एवं समन्वय जुड़े हुए होते हैं। बीते दशक की बैंकिंग भी इन ऐतिहासिक बदलावों, परिवर्तनों से अछूती नहीं रही है। यह बैंकिंग तकनीक में आए बदलाव का ही असर है कि आज बैंकिंग सेवा किस ी-न-किस ी रूप में 24x7 उपलब्ध है। इन बदलावों, परिवर्तनों से बैंकिंग सेवा में हर रोज नए बदलाव परिलक्षित हो रहे हैं, जिससे आम जनता के साथ-साथ देश की अर्थव्यवस्था भी लाभान्वि त हो रही है।

“If you owe your Bank manager a thousand pounds, you are at his mercy. If you owe him a million pounds, he is at your mercy”.

“If you owe your Bank manager a thousand pounds, you are at his mercy. If you owe him a million pounds, he is at your mercy”. Issue:

Issue: